The Demographic Time Bomb: How Our Assumptions About Global Population Are About to Go Bang!

Image by Gerd Altmann from Pixabay

It is a truth universally acknowledged that any article, blog or book about population growth should start with Thomas Malthus. This blog discusses a paradigm shift in world population – one which may finally put to bed the theories of the Rev Malthus, although that is far from the most important of the implications.

But let’s begin with Malthus. His Essay on the Principle of Population (first published in 1798) argued that there is a natural tendency for population to increase rapidly, and that population is held in check mainly by negative factors: hunger, disease and war. He went on to argue in later editions that preventive checks, such as later marriages, could ensure a higher standard of living, and increase economic stability.

At the time of the Essay’s publication, the population of the world is estimated to have been one billion. Today, the world’s population is over 7 billion. Over that period, the theories of Malthus have been kept at bay by rising living standards leading to longer life expectancy, reductions in infant (and maternal) mortality, near-eradication of many serious infectious diseases through vaccination and immunisation, better sanitation, and safer working conditions. The spurt in world population began in Europe and the USA, spreading to the rest of the world. As countries and regions have developed economically, they have acquired the means to ensure a better, healthier and safer life for their people.

The two centuries of rapid population growth have inspired various neo-Malthusian prophecies of doom – initially warnings of hunger and disease; and more recently warnings of the danger of exhausting the earth’s finite natural resources. Population has stubbornly continued to rise, and so have living standards, with billions being lifted out of absolute poverty in the last 30 years, in spite of the warnings of imminent doom. The neo-Malthusians have so far been proved wrong.

Checkmate for Malthus

This argument might continue as we move through the 21st century. But a new book calls into question the most fundamental – and hitherto unchallenged – part of Malthusian theory.

Whilst the world’s growing population bears witness of the ability of humankind to keep at bay the checks of hunger, disease and war, it has been generally assumed that the “natural tendency” for population to increase would continue. But the latest evidence shows that this is no longer a safe assumption.

In fact, it has been unsafe for some time, but the population explosion in the developing world, especially Asia, has masked a trend towards declining birth rates. The “reproduction rate” for human fertility – that is, the rate required to keep the population stable, all other things being equal – is 2.1. In 1950 the global fertility rate was 5.0. It is 2.5 today, and the latest UN projection is that it will be 1.9 by the end of this century.

The UN’s latest Population Projections, published in June of this year, suggest a median world population figure of 9.7 billion in 2050, and 10.9 billion in 2100. In other words, they see population growth continuing through the century but slowing down. Their lower projection is of a population of 9.4 billion in 2050, remaining the same in 2100 – in other words, in the second half of this century, we might see the end of global population growth.

The population is aging as well. In 1950 the median age of the world’s population was 24. Today it is 31. By the end of the century, the UN projections suggest that it will be 42.

In their book, Empty Planet: The Shock of Global Population Decline, Darrell Bricker and John Ibbotson go much further. They argue that the UN projections underestimate the factors that are driving population growth downwards. They argue that the global population in 2100 will be no higher than it was in 2000 and may even be lower. And the population will be older. They argue that factors such as economic prosperity, female emancipation, and urbanisation are leading women to exercise their right to have fewer children, or not have children at all.

This tendency is most evident in developed economies. Remember, the replacement rate for fertility is 2.1:

- The EU’s average fertility rate is 1.6

- The USA’s fertility rate is higher than Europe’s – 1.9. Bricker & Ibbotson argue that this, together with its relatively open immigration policy (at least for now), means that its population is projected to grow from 345 million today, to 450 million by the end of the century – this is consistent with the UN projections

- Japan’s fertility rate is 1.4. More than 25% of the population are of pensionable age. Median age is 48. Bricker and Ibbotson argue that Japan’s population will fall from 125 million in 2000 to just 83 million in 2100

- Other Asian “tigers” are following suit. South Korea, Singapore and Taiwan all have fertility rates around 1.2. Bricker and Ibbotson say that in the middle of this century, South Korea is set to overtake Japan as the “oldest” population on earth

- China’s population is set to peak in 2030 at 1.4 billion, but the average age will then increase rapidly, and the population is projected by the UN to decline to just over 1 billion in 2100 – Bricker & Ibbotson believe it will fall further – back below 1 billion

- India’s population is projected to continue to increase to 1.7 billion in 2060, and then begin to decline

The only region that will buck the trend will be Africa, which is set to grow from 800 million in 2000 to 2.5 billion by 2050, and projected to grow to 4.3 billion by 2100 (according to UN projections). 60% of its population is aged under 25. Increasingly Africa will be anomalous: it will be the “Young Continent” – as we have previously discussed in our Africa blogs.

There is no fundamental disagreement between the UN and Bricker & Ibbotson as to the drivers of population change. It is a matter of degree. Bricker & Ibbotson see the downward drivers as stronger than the UN does, and largely irreversible. The UN allows the possibility that countries that seek to do so will be able to raise their fertility rates. Bricker and Ibbotson argue that such initiatives tend to have short-lived success, and that long-term downward trends will then reassert themselves.

But the direction of travel remains the same – only the duration of the journey is at issue. Interestingly, the UN’s 2019 projections are slightly but significantly lower than the previous set, published in 2017. The trend raises some big questions – both intellectual ones for futurists, and practical ones for business strategists and economists.

- What does the projected decline and aging of China’s population do to the assumption that this will be the “Chinese century”? Will China enter the economic doldrums, as Japan has already done?

- Will Africa’s population growth and the youth of its population make it a rising economic power, or will it fall foul of those Malthusian “checks” of hunger, disease and war?

- Will Africa’s young people be welcomed by the rest of the world as a valuable resource, or seen as a mass-migration “problem”?

- Will the USA, and other countries or regions with open migration policies fare better than those with greater reluctance to accommodate cultural differences?

- Will countries with older populations be less inclined to spend, and more inclined to save for old age?

- Will countries with older populations be less inclined to fight wars, or will they simply fight by other means – drones and cyber warfare, for example?

- Will countries with older populations be less innovative and adaptable?

- Will falling population mean we have a greener planet?

- How will Governments balance the needs of older people with the expectations of people of working age?

- How will technology allow new opportunities to address these problems?

- Will countries seek to persuade (or coerce) women into having more babies? Will they succeed?

These 11 questions are a starter. Increasingly we can expect to see the demographic time-bomb baked into foresight frameworks and scenario planning exercises. And I am sure SAMI will have plenty to say about this.

If he could, what would Malthus be blogging?

Written by David Lye, SAMI Fellow and Director

The views expressed are those of the author and not necessarily of SAMI Consulting.

SAMI Consulting was founded in 1989 by Shell and St Andrews University. They have undertaken scenario planning projects for a wide range of UK and international organisations. Their core skill is providing the link between futures research and strategy.

If you enjoyed this blog from SAMI Consulting, the home of scenario planning, please sign up for our monthly newsletter at newreader@samiconsulting.co.uk and/or browse our website at http://www.samiconsulting.co.uk

CLIMATE CHANGE – CLIMATE EMERGENCY

One of the clearest “megatrends” facing the world must surely be climate change – or “climate emergency” as many commentators are now calling it. Clearly there are a range of outcomes possible, from the ambition of a “less than 1.5°C” level of global warming from pre-industrial levels, to frightening suggestions of an increase of 6°C or more. But whatever the outcome we can be certain there will be major ramifications for the world, its people and its flora and fauna. And for organisations of all kinds.

We’ve decided to focus on this major issue in a new series of blogposts. We will cover the likely impacts of climate change on various parts of the global ecosystem, and address both “mitigation” (reducing emissions) and “adaptation” (coping with climate change already happening).

The International Panel on Climate Change, set up in 1968, is the main international body attempting to get global agreement on ways of reducing climate change. It achieved a notable success in 2015 with the Paris agreement, signed up to by nearly 200 countries, including the USA and China, with most ratifying the agreement in April the following year. The agreement aims to respond to the global climate change threat by keeping a global temperature rise this century well below 2°Cabove pre-industrial levels and to pursue efforts to limit the temperature increase even further to1.5°C.

Unfortunately, the incoming Trump administration in the US announced on 1 June 2017, that the United States would withdraw from the agreement, with an effective withdrawal date of 4 November 2020.

An independent group, Climate Action Tracker, has analysed the pledges and policies put in place following the Paris Agreement, and it is clear that they are nowhere near the level necessary to hit the 1.5°C target, with 3°C being more likely – twice the target level.

So what would such a rise or worse actually mean? We shall look to answer that question in a number of areas:

- Climate change and the sea: sea-levels, acidification, coral bleaching, changing fish migration patterns

- Climate change and agriculture: pluses as well as minuses

- Impact of warming world on natural defences – methane sinks in Siberia, ice packs reflecting sunlight etc

- Extreme weather events

- Migration

What technologies could be effective in mitigating climate change? What upsides could there be?

- Renewables: solar/wind/tidal/bio/, progress, economics, battery storage

- Carbon capture and storage

- Transport: electric vehicles (including planes and ships), air taxis, Heathrow; commercialisation ofspace

- Other more innovative technology responses – cloud seeding

And what might the political and economic impacts be?

- Stern report 2006

- Future of fossil fuel industry: disinvestment, “keep it in the ground”, stranded assets, fracking

- Impact on finance sector – Bank of England warnings, insurance industry

- Political responses: new Green Deal, insulation, next COP event, street-level response; political impacts of climate change and climate change mitigation (including geo-political impacts on oil-producing countries)

Debate has focussed on achieving zero emissions by at least 2050, preferably earlier. But even achieving that is likely to be hugely disruptive, and we saw in a previous blog that BP’s energy forecasts show this to be unlikely. Recently the climate emergency had a moment at the centre of public debate (at least in the UK) with the visit of Greta Thunberg, David Attenborough’s powerful programme and the Extinction Rebellion disruption. And the Government has now committed to net zero carbon emissions by 2050.

If you have views on any of the issues in this field, please do contact us and we can give you the opportunity to express them.

Written by Huw Williams, SAMI Principal

The views expressed are those of the author and not necessarily of SAMI Consulting.

SAMI Consulting was founded in 1989 by Shell and St Andrews University. They have undertaken scenario planning projects for a wide range of UK and international organisations. Their core skill is providing the link between futures research and strategy.

If you enjoyed this blog from SAMI Consulting, the home of scenario planning, please sign up for our monthly newsletter at newreader@samiconsulting.co.uk and/or browse our website at http://www.samiconsulting.co.uk

In 2017-18, the private rented sector accounted for 4.5 million or 19% of households. Throughout the 1980s and 1990s, the proportion of private rented households was steady at around 10%. The sector has doubled in size since 2002 and the rate has hovered at around 20% since 2013-14.

25-34-year olds are now more likely to be private renters than owner occupiers. So if you look at the age range of 25 – 44 years, which is the majority of the IP (income protection) market for new customers, a very significant number are private renters. Despite this change anecdotal evidence suggests that only around 6.5% of IP customers are renters.

A significant proportion of them are pretty similar to those with mortgages. More than a third have at least one dependent child and most are working. Between 15 and 20% of rent arrears in the private rental sector can be put down to sickness.

So what happens when sickness strikes and a household doesn’t have IP? If the household is entitled to Universal Credit (UC) and they live in social housing their rent is normally met in full minus the “bedroom tax”. This is not the case for private renters. Here their eligible support is determined by Local Housing Allowance Rates (LHAs), which are pegged at the cheapest rent in an area for a particular size of property or capped. In addition, LHAs were frozen in 2016 until 2020 while private rental costs have gone up. A growing gap has been created by this system between the rent households have to pay and the amount of UC they receive for that purpose.

The gap is very variable. In most of London and some other UK hotspots the gap can be very large indeed and even in less well-off areas the gap is still significant. Here are five examples of the average monthly gap – Hounslow (£437); Cambridge (£531); Bristol (£217); Milton Keynes (£148) and York (£107). To meet the gap households have to find the extra money from the living expenses element of their UC. In 2017, 38% of private landlords experienced UC tenants going into rent arrears. Three out of 10 of those going into arrears were evicted. Homelessness has grown by 40% in the past five years. Apart from the financial impact of the gap there is also the social burden on families caused by relocation – often well away from their original homes. And as well as the short-term emotional disruption, the longer-term health and social consequences of homelessness can be significant, particularly for families with children.

For most customers, buying IP is a lifestyle choice not to be dependent on means-tested benefits from the State, having own occupation cover and rehabilitation support. For those in social housing this remains a situation of choice. For private renters the choice is starker. Either you have IP to cover your rent and living expenses, or you will not have sufficient money to pay your rent and support your family.

The growth of the gap is a strong incentive for IP purchase and is an opportunity for local intermediaries to get to know a new market, form relationships with tenants, letting agents and landlords to meet an ever-growing household resilience need. As with all IP advised sales documentation should include a warning with regard to the possible interaction between IP policies and State benefits and for rentals it may also be wise to document that the purpose of the product is to support rental payment and living expenses.

Written by Richard Walsh, SAMI Fellow and co-chair of BRHG, and originally published on the IPTF website, June 2019.

The views expressed are those of the author(s) and not necessarily of SAMI Consulting.

SAMI Consulting was founded in 1989 by Shell and St Andrews University. They have undertaken scenario planning projects for a wide range of UK and international organisations. Their core skill is providing the link between futures research and strategy.

If you enjoyed this blog from SAMI Consulting, the home of scenario planning, please sign up for our monthly newsletter at newreader@samiconsulting.co.uk and/or browse our website at http://www.samiconsulting.co.uk

AI: More Than Human

Image by Gordon Johnson from Pixabay

The Barbican exhibition on AI (running until 26thAugust) is a bold attempt to bring together cultural and scientific history, analysis of current technologies and issues, and examples of possible futures. When I visited it was certainly popular, with lots of young people enjoying playing with the exhibits.

The first section identified how over history there have been many cultural ideas about inanimate objects coming alive. This covered the Jewish Golem, Mary Shelley’s Frankenstein monster, Japanese Bunraku puppetry, through to more modern examples like Blade Runner.

More interestingly, in the second area, there was an extensive history of scientific thought into artificial intelligence. This covered “Stanford’s cart”, a 1960 attempt at an autonomous vehicle; basic principles such as Gödel’s Incompleteness Theorem; “expert systems” (an approach to AI now largely superseded); and on to a discussion about the Singularity, when AI becomes more than human. Unfortunately, because the place was so busy, it was difficult to go through all of the information presented, which seemed very comprehensive.

Another section explained the basic technology of modern AI – machine learning, deep learning, neural networks etc – with a number of interactive displays.

This section raised some of the common concerns about AI: biased decisions because of incomplete data, privacy and security, the relationship between humans and AI systems (empathetic or confrontational). One particular area was the use of AI by the military – autonomous weapons systems. Many people are unhappy with the idea of machines killing people with no human intervention and are now trying to get international agreements to ban such weapons, in the same way as we have bans on chemical weapons – stopkillerrobots.org. This seemed an oddly simplistic area – most people who have any interest in AI will already have come across these questions, and they weren’t explored in any depth.

Then there was a display devoted to AlphaGo, which raised the question of what it means to be creative. Does the fact that the system made an unexplained innovative move differ in any real sense from an expert’s (detective, surgeon) “gut instinct” – something built up over years’ of experience?

A section on the interaction of the biological world and AI explored how one could create environments that mimicked those of history or other planets, and how plant development could itself encode information – “endless evolution”. “A-life” explored how bio-mimicry could create new products and challenge ones’ perception of what was natural and what engineered. Some of the supporting information seemed over-ambitious however – “changing the nature of time”?

Down in the Barbican Pit was an immersive display – “What a Loving and Beautiful World”. Pretty images rolled around the four walls of the room, and by waving at them you could change how they behaved. It wasn’t all clear what the point of this was – when asked the assistant explained what it did, but not why.

Perhaps the best example of new robotic usefulness was the “MakrShakr” – an automated cocktail maker, but sadly, I didn’t get chance to sample its wares!

Written by Huw Williams, SAMI Principal

The views expressed are those of the author and not necessarily of SAMI Consulting.

SAMI Consulting was founded in 1989 by Shell and St Andrews University. They have undertaken scenario planning projects for a wide range of UK and international organisations. Their core skill is providing the link between futures research and strategy.

If you enjoyed this blog from SAMI Consulting, the home of scenario planning, please sign up for our monthly newsletter at newreader@samiconsulting.co.uk and/or browse our website at http://www.samiconsulting.co.uk

Are we entering a new age of medievalism?

Image by Rudy and Peter Skitterians from Pixabay

“People in this country,” said Michael Gove, former minister and now candidate for leader of Britain’s governing Conservative Party, “have had enough of experts.” And he certainly seems to have a point. The debate about Britain’s departure from the European Union has been replete with “experts” (the Bank of England, the Treasury, the IMF, the Confederation of British Industry, virtually every employer and so on), almost always on the Remain side. The other side of the debate is notable for its appeal to belief in the country, and a scorn of “Project Fear”. And that side won.

In the United States, the cry of “fake news” drowns out detail. President Trump proposes the shutdown of the National Endowment for the Arts and the National Endowment for the Humanities. On the internet, people who believe that vaccines cause MMR are promoting an anti-vaccine agenda in the face of mumps and measles outbreaks. Experts are derided. Science is ignored. Fact is prey to belief.

We have said before that the seeds of the future are to be found in the present and the past. To try and understand what this move to belief means, let’s look at the time when belief was indeed greater than fact: in the West, the medieval world of the 13th through 16th centuries. There are some disturbing analogies. Here’s a selection.

- We no longer believe in evidence. People build their views of the world from images created by others, with their own agendas. Paintings become Photoshop; messengers from afar and sermons in church become those news feeds we choose to follow because they agree with and reinforce our point of view.

- Holding contrary views is becoming dangerous, and we cannot risk exposing our young people to the pollution of conflicting ideas. In denying platforms to modern day heretics by, for instance, banning right wing speakers, it’s not hard to see iconoclasm and religious persecution.

- New technology spreads science and literacy and thought – and rumour and myth and false facts. Others have made the comparison between Gutenberg and Tim Berners-Lee, between the printing press and the world wide web, and they are right.

- We are under constant surveillance – or if we are not, we feel ourselves to be. Britain has the highest density of CCTV in the world; China has facial recognition built into (it seems) everything; Google, Apple and Facebook know who you are, intimately – and who your friends are. It’s a short step from this real surveillance to the stories of an omnipresent God, who knows all – and judges you for your actions as China’s concept of social capital judges you now.

- We are dependent on processes we don’t understand, cannot control, and for which we need intermediaries. In the Middle Ages, we propitiated against the ever present threats of war, famine, plague and death with our taxes and our tithes to the church; now our interconnected world is intertwined in ways which we are unable to understand or fix, and we pay our government and the private sector to make things work for us.

- And of course the ideological schism between faith and fact, between populism and western liberalism, between demagoguery and democracy, finds its comparators everywhere: from the Hundred Years war to the denials of Galileo, from the book burning of Savonarola to the attempted destruction of the libraries of Timbuktu.

The past may be a foreign country, but the map looks awfully familiar.

So is the future a medieval one? Maybe with some aspects of A Canticle for Liebowitz, as outposts of civilisation preserve the learnings of the past into the future? Are we going to see a slow slide back to the pre-Enlightenment?

It is too early to tell. Science and fact is putting up a fight. Under enormous pressure, online media giants are engaging more fact checkers. Candidates for the leadership of the Conservative Party are signing pledges which seem to control others campaigning for them (and hence spreading stories which may, or may not, be true). Billionaires are putting their money into spaceflight – the ultimate scientific endeavour. Whilst demagogues seem on the rise in the West, there is still, for now at least, the chance that elections will return their polar opposites and the dial will swing once again. The battle between fact and belief has returned to the public space: and the last time that happened, it led to the Enlightenment. It is equally possible that what seems like a turning point towards medievalism is in fact populism’s last gasp, and the turning point is towards a second Enlightenment.

The first Enlightenment, though, took a century to embed. There is no telling how long the second might take…..

Written by Jonathan Blanchard Smith, SAMI Fellow and Director and Martin Duckworth, SAMI Principal

The views expressed are those of the author and not necessarily of SAMI Consulting.

SAMI Consulting was founded in 1989 by Shell and St Andrews University. They have undertaken scenario planning projects for a wide range of UK and international organisations. Their core skill is providing the link between futures research and strategy.

If you enjoyed this blog from SAMI Consulting, the home of scenario planning, please sign up for our monthly newsletter at newreader@samiconsulting.co.uk and/or browse our website at http://www.samiconsulting.co.uk

In the first blog of this series, we set out a quick overview of the factors that might make Africa the most important continent by the end of this century. We then looked at the social and technological factors that would drive change in Africa. We now turn to Africa’s environmental opportunities and challenges.

There are three key environmental issues for Africa in the decades ahead:

- Climate change and its impact

- The Urban Environment as Africa’s population rapidly grows and migrates to towns, cities and “megacities”

- Africa’s unique natural environment and natural history

Climate Change

The latest IPCC (IntergovernmentalPanel on Climate Change) projections make worrying reading for Africa. They warn that temperature of 1.5% or 2% above pre-industrial global temperatures will adversely affect yields of maize, rice, wheat and other staples, and sub-Saharan Africa will be more prone to extreme temperatures and/or heatwaves.

More specifically, in Western Africa and the Sahel, the IPCC sees a projected increase in the likelihood of periods of drought. In Southern Africa also, it predicts lower rainfall over Namibia, Botswana, Northern Zimbabwe and Southern Zambia. In East Africa, the IPCC takes the view that rainfall may be higher in Somalia, but lower in Ethiopia.

The possibility of an increased frequency in adverse weather events, such as the typhoons that recently hit Mozambique, will further test Africa’s ability to respond and increase its resilience in the face of environmental challenges.

In a worst case, adverse impacts of climate change could see as many as 86 million migrants seeking to escape affected areas. To put this in perspective, in 2018 there were estimated to be 258 million migrants across the whole world.

Taken together these projections increase the risk of major disruption at a time when, all other things being equal, Africa would be growing and thriving as its population increases and the innovation it has already shown in technology continues to progress. Africa’s lack of infrastructure will make it harder to respond to natural disasters, as compared with, say North America or East Asia. Whilst there is a very rapid and widespread expansion under way of African infrastructure, which we will look at in the next blog in the series, Africa faces a major challenge in becoming more resilient.

In responding to the challenge, Africa will not only need to develop a stronger infrastructure, but innovate, for example in using different strains of cereal crops that are more resilient and/or better adapted to the changing natural environment.

It is manifestly in the interests of the rest of the world to assist Africa in its climate change and development goals. At the most basic level, Europe cannot handle unconstrained refugee flows; at the economic level, Africa represents a massive market to sustain future global growth. We see the realisation of these interests, and their embedding in the body politic of the West, to be highly important in providing funding and opportunities for Africa’s development; whilst at the same time being most subject to the resurgent populism currently enveloping the democratic world.

The Urban Environment

By 2050, the African population will be 2.4 billion, and, more strikingly, one third of the world’s youth population will be African, according to a report prepared for the EU Institute for Security Studies (ISS). This growth will be greatest in West, Central and East Africa. By the end of the 21stCentury, Africa’s population is projected to be over 4.1 billion. It will be the most populous continent on earth.

Today 60% of Africa’s population is rural. Urbanisation though will mean that this century’s massive population growth will inevitably see the rise of African megacities. By 2050, four of the world’s 20 most populous cities will be in Africa: Kinshasa (35 million), Lagos (32.6million), Khartoum (16 million), and Dar-es-Salaam (16 million).

Given the absence of modern infrastructure, the rapid growth of these cities presents an obvious and huge challenge to African governments. Will urban planning be possible? Dar-es-Salaam is seeking to apply planning, zoning, transport, sanitation, ensuring access to water, and tackling vulnerability to flooding.

As part of its Belt & Road investment in Africa, China will have plenty of practical advice on building cities. But the sheer pace of growth, the existence of rich and powerful vested interests, and the natural tendency of rural migrants to cluster together in shanty towns for reasons of economy and mutual protection make it likely that much of Africa’s urbanisation will be a crowded and chaotic journey.

However, as noted in previous blogs, urbanisation will also unleash Africa’s flair for innovation, for example in the use of technology. Africa’s evolving megacities will be interesting places, if not quiet ones.

Africa’s Natural Environment

Africa’s unique natural environment is under threat as never before. The struggle to protect species such as the African elephant and rhinoceros from poachers and trophy hunters has been documented for decades, as has the threat to primate species caught up in war zones, such as mountain gorillas in the Central African Highlands, or bonobos in the Democratic Republic of Congo. The International Union for Conservation of Nature (IUCN) declared lions to be vulnerable in 1996, and the African Wildlife Foundation reports a 43% decline in Africa’s lion population in the last 21 years, with lions “regionally extinct” in 15 countries.

There is much positive work being done to try to combat this:

- the recruitment of local people as guardians of their own local environment,

- sustainable land use,

- innovative use of technology in tracking and protection,

- breeding programmes,

- the economic benefits of eco-tourism, and

- the use of social media and other campaigning tools to dissuade trophy hunters and others who provide a market for poached animals and their parts.

However, Africa’s projected rapid population growth, potential environmental challenges from climate change, and rapid infrastructure development will all add to the pressure on Africa’s natural environment. Even if population growth centres on cities, the market for exploiting Africa’s wildlife through smuggled goods may increase.

There will be local disputes to be resolved as farmers affected by climate change, seek to move closer to nature reserves and/or animals seek to migrate from areas affected by drought.

As well as harnessing local efforts to protect the environment, the desire to manage and conserve will also be an international one, which will provide an opportunity for regional and pan-African collaboration and sharing of knowledge.

Watch This Space

In the next blog in this series we look at Africa’s economy, surveying what is driving change, and how Africa might take off into sustained growth in the coming decades.

Written by David Lye, SAMI Fellow and Director

The views expressed are those of the author and not necessarily of SAMI Consulting.

SAMI Consulting was founded in 1989 by Shell and St Andrews University. They have undertaken scenario planning projects for a wide range of UK and international organisations. Their core skill is providing the link between futures research and strategy.

If you enjoyed this blog from SAMI Consulting, the home of scenario planning, please sign up for our monthly newsletter at newreader@samiconsulting.co.uk and/or browse our website at http://www.samiconsulting.co.uk

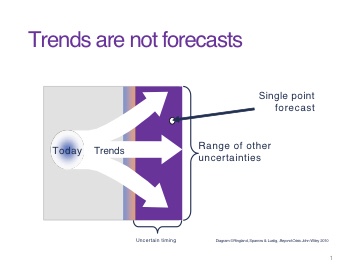

Megatrends and how to survive them – conclusions

Megatrends and How to Survive Them is the title of our book published by Cambridge Scholars Publishing and available on Amazon. This is the last of a series of blogs based on the work we have done for the book.

Our focus in the book was on global megatrends that would play out during the time span of an organisation’s planning. It wasn’t about the StarTrek, 100 year in the future type of predictions (or science fiction to be more exact).

Trends can emerge in many different ways; we have suggested a particular way that each megatrend might go. But, a reminder that trends are not forecasts!

A forecast is a single point in time, a prediction. Usually with a note of the percentage possibility to hit the prediction. Also it is usual that these forecasts are no more than 9-12 months in the future. Philip Tetlock ran a research project called “The Good Judgement Project” to see what sort of person could make good predictions. You can find out more about it in his book, Superforecasting: the art and science of prediction.

We had to make generalisations of each of the trend to keep them accessible. We supplied a list of questions (some of which we’ve repeated in the previous blogs) to help people to go deeper into each of the trends, to explore in more detail just how they might emerge and, indeed, what could disrupt them.

The underlying theme across all the trends is that an increasing number of people across the world are able to make choices – in life style, in where and how they live, in what they buy. These choices are driving innovation, society, technology and the economy, as well as impacting our global limits and climate.

Exploring these trends and how they might play out, however, is only a first step. There are several more before you can develop options, decide on a strategic direction and implement a new strategy.

We suggest three provisos:

- Beware of cognitive biases. There is plenty going on in peoples’ lives; cognitive biases help us to deal with information overload, lack of meaning, the need to act (react) quickly and they can help us to remember things. They are assumptions which we base thinking and decisions on.

- Be cognisant of the fact that many people find change threatening, so change management is needed. Change is facilitated by using images of the future which can be built to be relevant to your organisation and can be based upon these megatrends.

- Trends are not independent, they are part of complex systems, so when thinking about how to respond and what you might do to influence a particular trend, you need to consider it in the context of the larger system. Any action that you take may have delayed effects on one or another of the trends.

The most important thing that you can do with these trends is to explore them and stimulate a different sort of conversation, a different and deeper understanding of how they may affect your organisation and the work you do in the coming 10 – 15 years. And of course, what the opportunities (and risks) might be going forward.

The future is a foreign country – enjoy the exploration.

Written by Patricia Lustig, SAMI Associate and MD, LASA Insight, and Gill Ringland, SAMI Emeritus Fellow and Director, Ethical Reading.

The views expressed are those of the authors and not necessarily of SAMI Consulting.

SAMI Consulting was founded in 1989 by Shell and St Andrews University. They have undertaken scenario planning projects for a wide range of UK and international organisations. Their core skill is providing the link between futures research and strategy.

If you enjoyed this blog from SAMI Consulting, the home of scenario planning, please sign up for our monthly newsletter at newreader@samiconsulting.co.uk and/or browse our website at http://www.samiconsulting.co.uk

Risk management and the impact of culture

With so many examples of poor corporate behaviour and poor governance, it seemed a good time to address why getting the culture of an organisation right was so important. The CRSA (Control and Risk Self Assessment) Forum is an independent group ofenthusiastic practitioners and academics led by SAMI Fellow Professor Paul Moxey, and it used its recent meeting to explore culture and governance.

The day was kicked off by Simon Lowe of Grant Thornton describing the research they had done on culture and its role in effective governance, and their approach to auditing culture. He described how compliance with the UK Corporate Governance (UKCG) Code was improving, but it was now apparent that assessment needed to go beyond compliance to the application of the principles.

Good governance needs a proper understanding of risk – “the board should carry out a robust assessment of the company’s emerging and principal risks” (UKCG). Clearly technology is one major area of risk. However,from their analysis of company accounts, Grant Thornton found that, in several sectors – including,astonishingly the financial sector – many companies had not identified technology as a risk. And, of those that had, fewer than 30% had a board member with technology expertise.

Annual reports did contain references to corporate culture, but few CEOs (29%) referred to what they might do about it. Monitoring health and safety and running some employee engagement surveys seemed to be as far as it went. One or two examples of how culture might be captured in a “dashboard” were shown.

Then Simon’s colleague, Karen Brice, led an exercise on producing metrics for culture. She proposed a 6-factor “culture web” including such things as “rituals and routines”, “control systems” and “power structures”. The point of the exercise was not so much the absolute values assigned but the different perspectives different people’s assessments revealed.

The session generated an intense and lively discussion. There was some scepticism as to whether board members really wanted to get to grip with risks, preferring instead “plausible deniability” – several of the well-known governance disasters were explored. The challenges of creating common cultures following mergers were raised (an example being AT&T and HBO). And the idea of making the challenge a positive by promoting “Boardroom Brilliance” was also proposed.

The next session led by Peter Hanley and Colin Perris talked about “risk exploitation” and the work they were doing to formalise a process – even an app – to help with that. Their basic tenet was that a risk management approach tended to try to limit the forces pulling the organisation away from its goals. Instead what was needed was a focus on achieving the positive outcome. They too led us in an exercise, where we role-played being board members of a social housing organisation facing the post-Grenfell world. The exercise highlighted how easily one fell into considering risk as negative, rather then driving towards a positive. A key idea of a “Golden hour” emerged – pre-prepared mitigation strategies that would enable boards to react quickly to major challenges.

Later in the day SAMI Associate Garry Honey discussed creating a positive risk culture. Different people, even within the same organisation, will have different risk appetites, often depending on their role or inclination. A CFO is likely to be risk averse, while a hedge fund manager sees risk as an opportunity for higher profit. Garry explored the known/knowns and unknown/unknowns matrix, showing how best to expand the former area. He then went on to discuss reputation management, arguing the need for prevention rather than cure. Ultimately, he too was arguing that coping with risk was all about culture rather than process.

The day ended with a session by SAMI Emeritus Fellow Gill Ringland talking about the “Ethical Reading” (the place not the activity!) project she is involved with. Again the point was that compliance is not enough. In multi-cultural and fragmented societies, traditional norms and structures, and the support of the community can break down. So there needs to be a strong lead focus on common ethical principles, such as respect, co-operation, collaboration, integrity, fairness and responsibility. Happily, she had found many willing volunteers and champions to participate in promoting these ideas – see #itstartswithme. Her goal is to spread these ideas out into a much wider “Ethical cities” programme.

All in all it was a very inspiring day with loads of interaction and involvement of the audience. The value of scenarios in the consideration of risk came out strongly. One can but hope that the days of truly valuing and understanding the role of culture and ethics in organisational decision-making is coming that much closer.

Written by Huw Williams, SAMI Principal

The views expressed are those of the author and not necessarily of SAMI Consulting.

SAMI Consulting was founded in 1989 by Shell and St Andrews University. They have undertaken scenario planning projects for a wide range of UK and international organisations. Their core skill is providing the link between futures research and strategy.

If you enjoyed this blog from SAMI Consulting, the home of scenario planning, please sign up for our monthly newsletter at newreader@samiconsulting.co.uk and/or browse our website at http://www.samiconsulting.co.uk

Image by Gerd Altmann from Pixabay

Megatrends and How to Survive Them is the title of our book published by Cambridge Scholars Publishing and available on Amazon.

This is one of a series of blogs based on the work we have done for the book. We chose Biotechnology as a topic for discussion because over the next decade advances in biotechnology will “challenge what it means to be human” as reported in the Financial Times of 3rd December.

Biotechnology offers technological approaches for many of the health and resource-based problems facing the world. The application of biotechnology to primary industries, to healthcare, and to industrial processes, could result in a sizeable global “bioeconomy” by 2030.

There will be a lot of publicity about health applications – personalised medicine, gene editing, synthetic biology and direct neural interfaces, and the recent publicity on the gene edited Chinese twins is only the start. Biotechnology will have a massive effect beyond 2030 and the ethical implications will be much clearer.

However, it could be that the big opportunity will be around rethinking agriculture and the food chain, and industrial processes – saving energy.

Many of the potential advantages of biotechnology, such as salt-tolerant food crops, renewable energy sources like fuels based on algae, using organisms to neutralise or treat waste, and climate change mitigation, might happen faster than we think. A recent OECD report highlighted the role of bio-plastics for instance, in replacing those based on petroleum products.

Agri-business is big. Gene modification technology applied to animals and crops has created economies of scope and scale that have driven rapid corporate concentration. Genome editing – using CRISPR/Cas9 and tools to come – could become commonplace and lead to improved – and also to new – crops. Recent discussions on using DNA from fossils in the tundra to generate new life forms, raise the spectre of Jurassic Park.

| Jurassic Park

On a remote jungle island, genetic engineers have created a dinosaur game park. An astonishing technique for recovering and cloning dinosaur DNA has been discovered. Now one of mankind’s most thrilling fantasies has come true and the first dinosaurs that the Earth has seen in the time of man can emerge. But there is a dark side to the fantasy and after a catastrophe destroys the park’s defence systems, the scientists and tourists are left fighting for survival………. Source: Michael Crichton’s “Jurassic Park”. |

The main markets for biotechnology in primary industries (agriculture, forestry and fishing) could be in developing countries, due to the importance of primary production and industry to their economies.

There are a number of ventures developing food products using vegetable proteins to mimic more accurately the meaty, cheesy and creamy flavours of food derived from animal proteins. These products target the majority of meat-eating consumers, not just committed vegetarians. Using gene editing techniques to insert animal protein genes into food plants, offers the prospect of more convincing and delicious plant-based substitutes for animal proteins – “better than beef”.

If successful, these companies would create disruptive innovation across the human food chain, with profound consequences. As the ecological footprint of vegetable products is typically one tenth that of animal-based food, these innovations suggest the possibility of a sustainable path to feeding a global population exceeding 9 billion within our water limits.

Questions for leaders:

- How will agricultural/primary industries biotechnology affect you?

- How will health biotechnology affect you?

- How will industrial biotechnology affect you?

- How will you handle the ethical issues around employment and insurance cover which will be a side effect of genomic testing?

- How will you answer Millennials and other generations who will ask about the ethical issues of biotechnology in relation to your people and products and services?

We live in exciting times!

Written by Patricia Lustig, SAMI Associate and MD, LASA Insight, and Gill Ringland, SAMI Emeritus Fellow and Director, Ethical Reading.

The views expressed are those of the authors and not necessarily of SAMI Consulting.

SAMI Consulting was founded in 1989 by Shell and St Andrews University. They have undertaken scenario planning projects for a wide range of UK and international organisations. Their core skill is providing the link between futures research and strategy.

If you enjoyed this blog from SAMI Consulting, the home of scenario planning, please sign up for our monthly newsletter at newreader@samiconsulting.co.uk and/or browse our website at http://www.samiconsulting.co.uk

Activist Shareholders – Agents of Change?

- Photo by JESHOOTS.com from Pexels

Some people invest in a company because they trust the leadership to deliver shareholder value, due to track record and board composition. Some people invest in company because they like the product or service proposition, the basic business model. Activists invest for the latter and certainly not the former. Activists have faith in the underlying business but not the leadership, in fact an activist typically wants to replace the CEO, an impediment to releasing higher return for investors.

The activist takes a position from which to lobby other shareholders and their influencers, he is an agent of change and a disruptor, so to the board he is always an unwelcome intrusion. The activist takes on a significant challenge which, if successful, will bring substantial reward that is why he has a higher appetite for risk than the incumbent board and why he is invariably an aggressive hedge fund.

The first challenge he faces is to convince fellow shareholders that their trust in the incumbent board is misplaced and the business, having exhibited sluggish growth in a buoyant sector, is overdue for a new leader. In short it is time to call time on the CEO. If he manages to convince some shareholders of his defenestration strategy, there will be others who baulk at such drastic action.

The second challenge he faces is to convince fellow shareholders that he has a viable alternative to the existing CEO, a replacement who will adopt a new strategy to release value trapped within the business. Nervous fellow shareholders will be wary that to endorse the candidacy of the activists’ man could be simply of jumping from the frying pan into the fire and may not result in anything more than unnecessary upheaval. The status quo is a powerful advocate of inertia.

The third challenge he faces is to win a confidence vote at the AGM, by a significant majority ie over 50% and the size of some individual shareholdings might make this almost impossible. The activist will also aim to win over proxy voting agencies to his proposal, but not all agencies will be open to change. For example, pension funds tend be quite conservative and see any external pressure to impose new leadership as a risk to their long-term investment strategy.

The fourth challenge for an activist is to be patient as even a lost motion at an AGM can sow the seeds of discontent which come to fruition months or years later. Look at Premier Foods from July 2018 to date. At the AGM on 18 July 2018 the Hong Kong based activist and minority shareholder (10%) Oasis called a vote of no confidence in the CEO with a proposal to replace him with the Finance Director and a new strategy of asset disposal to release value.

The incumbent board presented the activist as an asset stripper.‘If these activist investors succeed in removing him, they risk destroying significant value, rather than creating it’ said former head of Waitrose Mark Price. The motion duly failed by 59% – 41% votes but having achieved support from well over a third of all shareholders, the proposal had achieved consideration. This despite the Chair rallying support for his CEO from the largest shareholder, Japanese Nissin Foods (20%).

In November 2018 the CEO surprised the market by announcing he would step down in three months so a successor could be found to pursue a new strategy. This appears to be by ‘mutual agreement’ but no doubt the confidence vote had some bearing. Two months later the UK activist Paulson increased its share from 7% to just under 12% suggesting that the CEO departure was a positive move, and there was indeed latent value in the business awaiting release. This seems to vindicate the Oasis AGM motion last July, despite it failing to succeed at the time.

Activists are truly agents of change, welcome or not, they make an impact even if it is just not always immediate.

Written by Garry Honey, founder of Better Boards, CEO, Chiron Reputation Risk and SAMI Associate.

The views expressed are those of the author and not necessarily of SAMI Consulting.

SAMI Consulting was founded in 1989 by Shell and St Andrews University. They have undertaken scenario planning projects for a wide range of UK and international organisations. Their core skill is providing the link between futures research and strategy.

If you enjoyed this blog from SAMI Consulting, the home of scenario planning, please sign up for our monthly newsletter at newreader@samiconsulting.co.uk and/or browse our website at http://www.samiconsulting.co.uk